The Simple 50/30/20 Budget Rule: How to Take Control of Your Finances

Struggling with money management? The 50/30/20 Budget Rule is the simplest way to take control of your finances, build savings, and enjoy life without financial stress. In this post, learn how to apply this powerful budgeting method to your own life and set yourself up for long-term financial success. 🚀

FINANCIAL LITERACY FOR ALL

Christopher Skyler

11/7/20243 min read

Why Most People Struggle with Money (And How a Simple Formula Can Fix It)

Managing money shouldn’t feel complicated—yet so many people struggle to save, invest, or break out of financial stress.

📌 The problem? Most people don’t have a system for managing their money.

They spend what they earn without a clear plan, leaving them:

💸 Living paycheck to paycheck with no savings.

💳 Drowning in debt because of impulse spending.

⏳ Delaying investing because they feel they “can’t afford it.”

The solution? The 50/30/20 Budget Rule.

It’s one of the simplest, most effective budgeting strategies to help you take control of your money—without feeling restricted.

In this article, you’ll learn:

✅ How the 50/30/20 Rule works and why it’s so powerful.

✅ How to apply it to your finances—step by step.

✅ How to adjust the rule for your personal goals.

Let’s dive in.

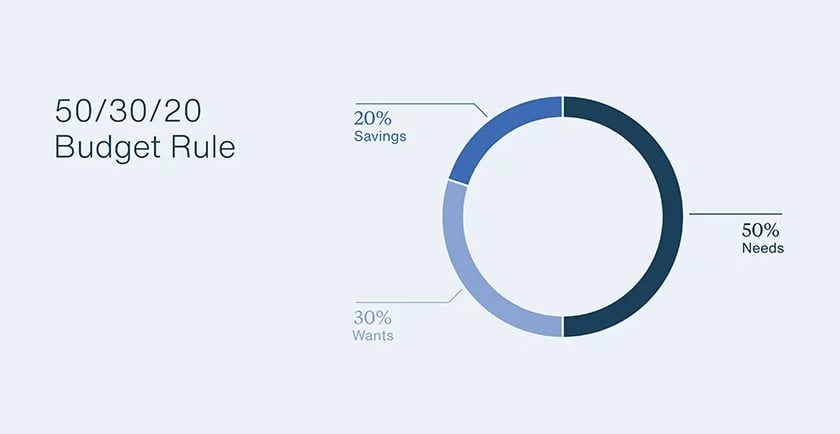

1. What is the 50/30/20 Budget Rule?

📌 The 50/30/20 rule is a simple way to divide your income into three categories:

50% for Needs (essentials like rent, food, and bills).

30% for Wants (entertainment, dining out, hobbies).

20% for Savings & Investments (building wealth and financial security).

💡 Why this works:

✔️ It keeps spending balanced—you cover essentials, enjoy life, and still build wealth.

✔️ It removes guilt—you can spend on things you love without feeling bad.

✔️ It ensures consistent saving—so you’re not waiting for “extra” money to invest.

👉 Think of it as the financial “diet” that actually works—sustainable, flexible, and effective.

2. How to Apply the 50/30/20 Rule (Step by Step)

Step 1: Calculate Your After-Tax Income

📌 Use your “take-home pay” (after taxes and deductions).

💡 If you’re self-employed, subtract estimated taxes first.

📌 Example:

You earn $5,000/month after taxes.

You split it into:

✅ $2,500 for Needs (50%)

✅ $1,500 for Wants (30%)

✅ $1,000 for Savings & Investments (20%)

👉 Once you know your budget, you can plan where every dollar goes.

Step 2: Allocate 50% to “Needs” (Essentials Only!)

📌 Needs = Expenses you MUST pay to live and work.

✔️ Rent or mortgage

✔️ Groceries

✔️ Utility bills (electricity, water, internet)

✔️ Health insurance

✔️ Transportation (gas, car payment, public transit)

✔️ Minimum debt payments

🔴 What’s NOT a “Need”?

❌ Eating out

❌ Netflix, Spotify, subscriptions

❌ Shopping for new clothes

👉 If “Needs” take up more than 50%, find ways to reduce costs (downsizing, refinancing, meal prepping, etc.).

Step 3: Allocate 30% to “Wants” (Enjoy Life—But Within Limits!)

📌 Wants = Non-essential expenses that make life fun.

✔️ Eating out & coffee runs

✔️ Shopping (clothes, gadgets, hobbies)

✔️ Gym memberships, streaming services, entertainment

✔️ Travel, vacations

✔️ Upgrades (new phone, premium subscriptions)

💡 The key? Spend on things you truly VALUE, not just out of habit.

🔴 Avoid the “lifestyle inflation” trap—don’t spend more just because you earn more.

👉 Enjoy your money—but with a plan!

Step 4: Allocate 20% to “Savings & Investments” (Building Your Future)

📌 This is the most important category—it’s what makes you wealthy.

✔️ Emergency fund (3-6 months of expenses)

✔️ Retirement savings (401(k), IRA, Roth IRA)

✔️ Investing (Stocks, ETFs, Index Funds)

✔️ Paying off extra debt

💡 Why this 20% is powerful:

✔️ Saves you from financial disasters (emergency fund = no credit card debt).

✔️ Grows your wealth automatically (investing lets your money work for you).

✔️ Makes you financially independent (so you’re not trapped in a paycheck-to-paycheck cycle).

👉 Think of this as paying your “future self.”

3. Adjusting the 50/30/20 Rule for Your Goals

📌 The rule is flexible—adjust it based on your financial situation.

🔹 If you have high debt:

✅ Do 40/20/40 instead (40% Needs, 20% Wants, 40% Debt Payoff & Savings).

🔹 If you want to build wealth faster:

✅ Cut Wants to 20% and invest 30% instead.

🔹 If you’re living in a high-cost area:

✅ You might need 60% for Needs, so adjust Wants & Savings accordingly.

💡 The key is to use this rule as a guideline—not a strict rule.

👉 Your budget should serve YOU, not the other way around.

4. Why the 50/30/20 Rule Works (And Why Other Budgets Fail)

📌 Why this budget works:

✅ It’s simple – No complex spreadsheets or tracking every dollar.

✅ It’s balanced – Covers needs, wants, and wealth-building.

✅ It’s sustainable – Unlike extreme budgets that feel restrictive.

🔴 Why most budgets fail:

❌ Too strict (people quit when they feel deprived).

❌ Too complicated (tracking every penny is exhausting).

❌ No room for fun (which leads to impulse spending).

💡 The 50/30/20 rule works because it’s easy to follow and maintain.

👉 A budget only works if you can stick to it.

Final Thoughts: Take Control of Your Money Today

📌 Your budget determines whether you stay broke or build wealth.

🚀 How to Take Action Today:

✅ Calculate your after-tax income and apply the 50/30/20 rule.

✅ Adjust your spending so Needs, Wants, and Savings are balanced.

✅ Set up automatic savings & investing—pay yourself first!

✅ Track your spending for 30 days to stay on top of your finances.

💡 Want a complete step-by-step guide to managing your money?

📖 Get your copy of Financial Literacy for All and start building wealth today!

© 2025 SkylerPublishing.com. All rights reserved.